Why we should change our money

What are the consequences of using our current system?

We are in trouble. We cannot live up to the goals stated in our Constitution’s first paragraph:

We the People of the United States, in Order to form a more perfect Union, establish Justice, insure domestic Tranquility, provide for the common defense, promote the general Welfare, and secure the Blessings of Liberty to ourselves and our Posterity, do ordain and establish this constitution of the United States of America.

Our current money system has unfortunate consequences that are not congruent with our Constitution’s goals. A private debt-money system is unsustainable – economically, socially, and environmentally. It is biased, and undemocratic. It transfers wealth from the many to the few, exponentially increases debt, limits economic diversity, and causes higher taxation.

Our money system transfers significant wealth from the many to the few, and creates human conflict as people compete for artificially scarce money and resources.

Over time, whoever controls the money system controls the nation.

The burdens of our current money system

ECONOMIC – It’s bad for business.

- Inflation and an unstable marketplace

- Not enough money on Main Street

- Too much debt

- Too many taxes

SOCIAL – The general welfare declines.

- Poverty and inequality increase

- No democracy

- No true justice

- No domestic tranquility

- Special interest defense instead of common defense

- Freedom is compromised & Liberty is insecure

ENVIRONMENTAL – We’re destroying our planet.

- Killing ourselves

- Killing other species

- Killing the planet

In sum, our money system destroys diversity – the condition of difference necessary to all life and creativity – in our economy, society, and environment.2

Economic burdens of our current system

It’s bad for business

- Inflation and an unstable marketplace

- Not enough money on Main Street

- Too much debt

- Too many taxes

Our money system is bad for business and competition. The fluctuating value of money, the necessity to borrow, and the high interest charges add risk to doing business. This is a greater hardship for smaller businesses that do not have the financial girth to protect themselves. And it encourages speculators into stock manipulations and hostile takeovers that run up prices and create hardships for all businesses.

An unstable marketplace

Our current money system creates recurring booms and busts by infusing too much new money into the economy and then completely shutting off money creation and shrinking the supply.

Businesses, employees, and customers suffer through no fault of their own.

When bankers are confident and think there is money to be made, they lower loan standards and create too much money. This new money is lent into a few sectors that are doing well because they can collateralize loans. This creates a boom in an asset class such as family homes, stocks, bonds, gold, oil and gas. The related businesses boom as well. A boom raises the value of the collateral so the banks can loan even more. The value becomes unsustainable as fewer and fewer people can afford the very high prices. Loans start defaulting, lowering the value of collateral as everyone starts to sell to pay back their loans. The many delinquencies force the banks to severely slow the lending that creates our money supply. Then the banking industry substantially raises qualifications when it is too late. Banks finally turn off the new loans because of higher risk levels, defaults, or less collateral. The early-in, early out speculators thrive. But many entering late, which is usually the general public, get hurt.

When borrowing drops dramatically, so does the money supply. There isn’t enough money in the system so prices go down (each dollar can purchase more), pushing more businesses out of the marketplace (called deflation). In the depressions that follow a boom, it’s impossible for many businesses to survive. Many people lose their jobs and customers are scarce. Even local and regional banks struggle to stay above water. As businesses die, choice suffers, employment declines, and communities despair.

The housing bubble that peaked in 2006, the consequent 2007 financial crash, and the Great Recession from 2007–2009 are a perfect example. In the last 40 years we have seen it over and over again in commercial real estate, oil & gas, stock market and single family housing. Since 1913, there have been 19 recessions, including the Great Depression of 1929–1933, and the Great Recession from 2007–2009.

These economy-wide booms and busts should be labeled a monetary cycle – they happen because our money system creates too much money, then reduces the supply and access to money. There can only be a business cycle for an individual product, company or industry, not the entire U.S. economy.

Unpredictable declining value of money – inflation!

Our money is constantly decreasing in value at unpredictable rates. Today’s system intentionally increases the money supply beyond the needs of population increase, greater productivity, and interest for the bankers. Its goal is to create too much money supply for the amount of domestically available goods and services – enough to steadily decrease the value (or purchasing power) of money by 2 percent each year and avoid deflation-recession. This is called inflation and it benefits some and not others. Our money system today is inflationary by design.

The bankers’ central bank is under constant pressure to find ways to counter the system’s tendency to over expand the money supply. (In the U.S., this is the Fed.) It must work to avoid excess inflation, runs on banks, and systemic meltdown. It is a difficult task. And while they deserve a tip of the hat because we have avoided the kind of hyperinflation that has occurred in other nations, the Federal Reserve System has done a poor job of meeting its 2 percent goal. Over their first 100 years, the value of money decreased annually at rates swinging from -1 to 12 percent by official tally (the Fed and Bureau of Labor Statistics) and by as much as 15 to 20 percent by alternative measures.3 These swings in the value of money benefit a few speculators, but they make life hard for Main Street, small business and farms, and consumers.

Not enough money on Main Street

Too much speculation

When a market swings widely, speculation thrives. Some speculation is good. It adds buyers and sellers to the marketplace. But when the marketplace is overwhelmed with speculators, the price of everything is run up. This is hard on the people and businesses who genuinely want to use products but cannot afford the payments and the higher asset prices. Today by many estimates 80 to 95 percent of trades on our currency, stock, and commodity markets are by high-speed speculators, extracting a bit of profit and running the prices up – holding trades for a few seconds on average.4 This is gaming, not productive investment. It shifts wealth from Main Street to Wall Street.

Today, most new money loans go toward speculation on residential or nonresidential mortgages and for speculative acquisitions by large companies, derivatives, and high speed Wall Street trading departments. Main Street businesses get less and less of new money loans.

Not enough competition

Our banker debt-credit money system concentrates wealth on Wall Street. Financiers have the money to buy up companies and other property, consolidate industries, limit new entries, and cripple competition. This creates monopolies and oligopolies. Our marketplace loses healthy diversity. Our small businesses and family farms don’t survive. For customers, this can mean higher prices and lesser product quality. Or, it can mean lower prices, but less money circulating in their local community, which ultimately compromises the tax base and the general welfare.

For entrepreneurs, it is harder to bring new ideas to market. Innovation suffers because only a small number of people have the wherewithal to invest, and only their choices make it beyond the design board. Small business faces burdens that big business can flick off its shoulders, tilting the playing field and making it harder for small business and entrepreneurs with innovative ideas to succeed. This reduces the number of competitive alternatives that keep an economy vibrant and dynamic.

Inadequate long-range planning and investment

Our money system demands quick growth and results. This means long-range investing is sidelined so that quarterly short-term profits can shine – sometimes foregoing larger long term profits that could be made by investing to stay in business longer. We do poorly at long-range planning, which often involves investments that may not pay off for decades – if at all in terms of direct profits for private industry. This is neither the most successful way to do business nor the best way to prepare our nation for our grandchildren’s futures – especially facing the dire consequences of climate change, increasing negatives of globalization, and the arriving robotic age.

Debt created money creates too much debt

Creating the money supply in our existing system requires an exponentially growing debt. A heavy burden of debt drags on our economy. Our nation is currently burdened with about $73 trillion in public and private debt, while the GDP – all the money changing hands in a year – is only $21 trillion. So, like musical chairs, there is economic conflict as people try to find the money to pay back their loans and interest. The many grow poorer and need to borrow, and the rich get richer and have money to lend or spend. Human conflict follows. The increasing and excessive debt carried by individuals, businesses, towns, cities, and the federal government saddles our citizens, businesses, and our future with an impossible burden.

Debt is not dangerous if it is used properly. Businesses benefit when they borrow to invest in equipment, new facilities, or other capital investments. It is a burden to business when they over borrow to buy other businesses, or borrow to stay in business, because they will not be able to repay their debt. It can lead to bankruptcy. Individuals benefit when they can borrow within their budget to cover emergencies and long term expenses like tuition, a home, car, or flat-screen TV. But, many have to borrow just to cover their daily business or living expenses. This is disaster waiting to happen.

Too much taxation

Under current law, our government cannot create money. When our government spends more than it receives in taxes, it must borrow. It must exchange a government IOU – a Treasury bill, note, or bond – for existing money that is already in circulation and in surplus for its owner. We the taxpayers then pay interest to these bond holders. In 2018 we collected $2,103 billion for government operating income. Out of that, $357 billion – or 17% – went to pay interest on this public debt. We paid another $99 billion – 5% – in interest to government trust funds.5 The interest rate on government debt averaged 2.6 percent. While our government can borrow as much as Congress allows it to borrow, which has historically been a steadily increasing “debt ceiling,” it is not creating money.

In our current system, our government guarantees our money with the full faith, credit, and shared wealth of the nation. Our government pays the cost of assuring that our money tokens are authentic and trustworthy by fighting counterfeiting. Our government pays for global military activities used to maintain our existing money system and the elite who benefit from it. We pay to supervise, hold accountable, and bail out the banks. We socialize the costs of money system maintenance and privatize the profits and benefits.

Why does the Government borrow money and make taxpayers pay interest on it, when government could create money for free?

Social burdens of our current money system

The general welfare declines

- Poverty and inequality increase

- No democracy

- No true Justice

- No domestic tranquility

- Special interest defense instead of common defense

- Freedom is compromised & Liberty is insecure

The general welfare was important to our founding politicians. It is mentioned twice

in our Constitution (in the first paragraph and in Article 1 Section 8). However, because our Congress ceded the power to create our money to private bankers, the general welfare has suffered as the financial sector favors its own private interests.

We have a century old slow and crippled rail network, bridges collapsing, potholes, high-priced communication networks, poor health, and inadequate access to quality education. The general welfare is suffering. This is not a good formula for creating quality customers, clients, consumers, and citizens.

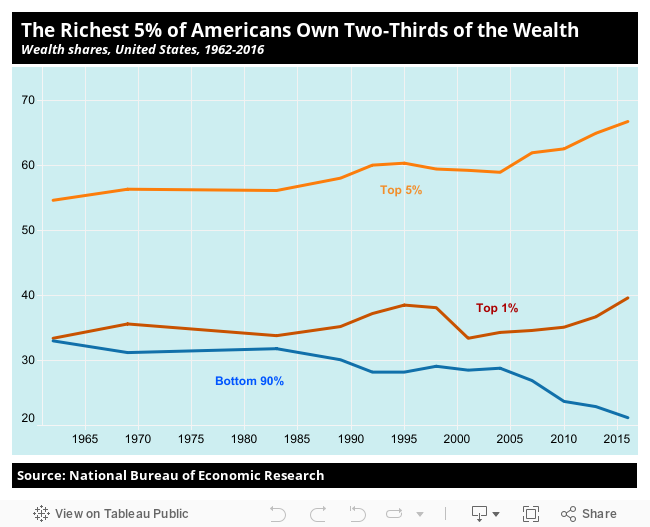

Increasing poverty and inequality

Our current system increases inequality by transferring wealth from the many borrowers to the few lenders. Money created by the commercial banks at almost no cost requires interest payments from consumers, businesses, and local communities. This shifts wealth from the productive economy to the financial sector, and increases inequality. It tilts the playing field toward the banking sector, and away from most of us. Our money system also sets a target of 3–5 percent unemployment; some people are intentionally left out and in poverty. Yes, some people make it up the steep incline and succeed, but we want far more to succeed. Too many are overcome by the disadvantages that the money system imposes and sink into poverty and despair.

Wealth inequality has been growing steadily and today it is greater than before the 1929 Crash and the Great Depression. In 2017, the three richest men in the U.S., Jeff Bezos, Bill Gates, and Warren Buffett, owned $249 billion in wealth between them – more than the combined wealth of the 160 million poorest Americans – half our population! This is radical inequality. By 2018, the wealth of these three men had ballooned to $330 billion. This disparity and the number of poor and homeless are growing at unsustainable exponential rates.

This suffering is a choice. The Age of Scarcity is over. We have the ability to meet the basic needs for all humanity. Not everyone will live in a mansion, but providing food, healthcare, education, shelter, and clothing for all is within our means. A scarcity of money stops us – as does our thinking that paying for a better future cannot be done!

Radical inequality is bad for business; it reduces the number of customers, crippling local businesses. Radical inequality is a recipe for famine, war, ecological disaster, and the end of life as we know it. It creates strife and takes us in the opposite direction from “a more perfect Union.”

Our democratic republic is dysfunctional

Today our democracy is at risk. On the 2018 Economist’s Democracy Index, the U.S. ranks #25 – a “flawed democracy.” Today we cannot make the decisions we would make in the open, issue-based, representative, democratic-republican form of government that our Constitution intended. This is partly the result of misunderstanding how money works and its significant role in influencing society.

Bad decision-making

We all want to see a thriving economy and high standard of living. But no matter what party has been in power, we’ve been unable to have a thriving economy that endures. Too many of our citizens do not share in the high standard of living we are capable of producing. Why is that?

It is because our leaders and representatives are not in control of the major influence on our economy – the money system and the amount of money in the supply. Money in circulation is the life blood of the economy. A quality economy needs to have money flowing and decisions about its use diversified in many hands. Instead, the 1913 Federal Reserve Act set up a system in which a very small sector of bankers with similar mindsets make the decisions that determine our well-being. Any kind of groupthinkers have blinders. Blinders stand in the way of good problem-solving and decision-making.

Influence and control of our society

Our money supply comes into being by the choices of private bankers; they choose who gets the money-creating loans. Their choices determine the money supply, policy, and the direction of investment and development.

The ability to create money is an advantage accorded no other business. Commercial banks and the financial sector that is owned by the banks do not do business on a level playing field; they control the field, make the rules, and tend to come out the overall winners. Their highest priority is bank profits, not the well-being of society and the economy. All other businesses and government are at a disadvantage.

All aspects of our society are heavily influenced by the choices of our financial elite. With an increasingly disproportionate share of our wealth, a small number of very wealthy people buy the educational and thinking institutions and control the ideas and policies that come out of them. They own the media and control public attention and discourse. They buy the election of legislative members, through lobbyists and campaign contributions, who do their bidding and pass the policies they want. We have to beg for their willingness to invest in transformative technologies and for their charity to do right by our citizens and communities.

Feelings of powerlessness

Most Americans justifiably feel that their voice does not count. Research says it doesn’t. People with money who donate to candidates are heard; people who cannot donate are not heard.6 Powerlessness leads to apathy, which leads to a lack of diversity in decision-making, which results in poorer decisions with poorer outcomes. In 2016, only 56 percent of our voting-age population voted in the presidential election. Roughly 40 percent vote in in-between elections, and even fewer for local elections. This is far from a functioning perfect Union.

No true Justice

When the money system gives special privileges to a tiny elite, there can be no equal justice under the law. A tiny super-rich elite buy law school curriculums and professors. They buy armies of lawyers to avoid civic responsibility and its consequences. When a wealthy elite can buy a blind eye to unfairness, buy leniency for their exploitation of labor and their degradation of the environment, and turn the justice system into a profit center, true Justice cannot be established.

No domestic Tranquility

We are not a tranquil nation. Over 12 percent of us go to bed hungry – 20 percent of families with children. One in eight of us over 12 are taking anti-depressants. One in five of our children have some kind of developmental problem. We have a one in three chance of getting cancer, and a one in five chance of dying from it. Nearly 40,000 people die from guns every year. From January to May 2018 more school children in the U.S. died from gun violence than U.S. soldiers in combat zones. Another 70,000 people die from drug overdoses. We have 5 percent of the world’s population and 20 percent of the world’s prisoners are incarcerated in the U.S. We are a stressed and unhappy nation – with seething anger over injustice, inequality, and the despair of powerlessness to make effective change.

Our current money system divides and rules us, pitting people against each other so that we don’t see our common cause. It creates false scarcities, pushing us to grab what we can when we can – stressing us all out. Our culture celebrates those who achieve wealth – even those who achieve it by exploiting and cheating others. Our culture idolizes the wealthy and disdains the poor – even the poor deliberately created by the system. All of this is a recipe for a poor economy, increasing discord, and ultimately crime and violence.

Defending special interests

We currently spend more on defense than the next ten biggest spending countries combined. And many of these countries are our allies. Our Congress puts money in the pockets of the defense industry in the name of jobs – and at the bidding of defense industry shareholders. Then we use our military might to protect specific wealthy interests, as if their interests are the nation’s interests. For example, we went to war in Iraq to protect the fossil fuel industry. We’ve been fighting for fossil fuel access even though our Pentagon has been saying for years that climate change is a threat multiplier and an “immediate risk to national security” and it’s time to switch to renewable energy.7 We went to war in Libya to protect the global banking sector.8 The people with the power to create our money have been using it to promote their own interests, not the interests of the nation.

Our current money system demands continuously increasing the size of the economy and maximizing profits. This has meant acquiring increasing amounts of nonrenewable resources from other countries and minimizing the cost. We’ve used our military might to assure cheap and underpriced global resources, subsidizing some business interests at the expense of continuous war. Lives are taken to assure cheap resources, increasing the likelihood of further conflict.

If we’d been defending the commons we’d listen to our military and we’d be spending our defense money differently. We would have spent more paying our soldiers well, training them at the highest level possible, and taking good care of those who give their health, well-being, and lives. We would not have hundreds of thousands of our veterans on the streets and homeless every year, while defense contractors building weapons deemed useless by our military experts take home billions in profits.9 We would have invested more in renewable energy instead of subsidizing fossil fuels, and we would not be defending a monetary system that shifts wealth from the many to the few. The resulting wars, poverty, and rising inequality creates global strife.

Freedom is compromised & our Liberty is NOT secure

Liberty is about freedom to choose. When the money system allows the banks to create, risk, and invest our money without our knowledge or choice, we are less free.

Liberty is about having an equal voice in public decisions. A democratic republic is not perfect, but so far, it is the best form of government. The decision to give private bankers the power to create money, gave an elite rich, in effect, the power to effectively rule over us. Our democratic republic is on life-support, with daily insults to the Constitution, the rule of law, and our Liberty.

Liberty is about responsibility and accountability to the community. True Liberty balances freedom with responsibility. Because wealth has overwhelming power in our society, it demands a waiver from responsibility and gets it. A big corporation can kill you with its pollution and get a financial slap on the wrist – or simply be excused as a job and shareholder-profit provider. We can’t all move to the places where the air is clean, the water safe, the food free from toxins, the streets secure, and the jobs provide a living wage. Many of us do not have this choice. When we have no choice, we are not free and our Liberty is lost.

Environmental burdens of our current money

We’re destroying our habitat, species, and our lives

- Killing ourselves

- Killing other species

- Killing the planet

We are causing illness and early deaths. Our health is in unnecessary jeopardy. Our life span is growing shorter. About 40 percent of us will get cancer in our lifetime, and 21 percent of us will die of it. People with cancer, even with insurance, are twice as likely to go into debt and declare bankruptcy. Bankruptcies create ripples of hardship in families, communities, and businesses.

We have more babies dying than any other developed country, and about one in five of our children has some kind of developmental difficulty or delay due to the toxic pollution in our environment. Sperm counts in men around the world have dropped by more than 50 percent in less than 40 years – signaling a decrease in health and a potential decline in fertility. The money system dictates that growth and short-term profits are a higher priority than life itself.

Killing other species

We have put all of life as we know it in jeopardy. Scientists estimate that we are pushing species to extinction at many times the natural rate, compromising entire ecosystems. According to the Center for Biological Diversity, extinction is a natural phenomenon and occurs at a natural rate of about one to five species per year. Scientists estimate we’re now losing species at up to 1,000 times the natural rate, with dozens going extinct every day.10

Killing our planet – Infinite growth on a finite planet

In our current system, borrowing must increase, so buying and selling must increase. To keep up, we increase production, population, and productivity. To feed this insatiable demand for increase, we deplete or pollute natural resources, and encourage population increase. We build and produce more and more. We buy more and more. We waste more and more. We pour money into the black hole of continuous war. A growing bigger economy becomes our goal, rather than a growing better, and healthier, and more caring economy. We can’t stop and think about prudent resource management because we need nonrenewable natural resources for continuous growth. It is not a sustainable system.

Our current money system requires using up nonrenewable natural resources at a faster and faster rate – and that’s what we’ve been doing. Our water aquifers are shrinking faster than they are refilled by nature. Our farmers, our soil, and farm land are at risk. Exploitation and degradation increase to serve the growth imperative of this system. Technology can help with bandages to slow degradation down. But, it can’t stop it unless we have more money to invest in sustainable solutions. Within our current money system, it is nearly impossible to make the changes necessary to maintain healthy human life on Earth.

According to most of the world’s scientists, we have roughly 10 years to change our behavior from exploitation, degradation, and destruction to renewable, sustainable, and stewardship.

So, what can we do?

Change the money; change the world

We can have a money system in which our government uses the democratic process established by our Constitution to create our money supply as an asset to the economy and society, rather than as debt to the private bankers. Then we will have the money and the power to achieve the goals set forth in our Constitution.

Thank you for reading this page. Please share then visit our take action page and help us spread the word. We can pay for a better world for yourself, your family and future generations. It’s time for Just Money now.

Previous Next: What is Just Money? ⇒

Comments

Ask a question or post a comment below; we love your feedback!

A project of Great Democracy Media, Inc.

Endorsed and supported by The Alliance for Just Money

Copyright © 2019–2026 by Great Democracy Media, Inc.

The materials on this site are licensed under a Creative Commons Attribution-NonCommercial-Sharealike 4.0 International Creative Commons License.